The global Internet of Things (IoT) market is projected to surpass $1.3 trillion by 2026, with banking and financial services emerging as one of the fastest-growing sectors for adoption. As customer expectations rise and competition intensifies, banks are turning to IoT banking software development to deliver more secure, personalized, and efficient services.

At its core, IoT in banking refers to the integration of smart devices, sensors, and data analytics into financial operations. From connected ATMs that self-diagnose maintenance issues to wearable devices enabling contactless payments, the Internet of Things in banking is redefining how financial institutions interact with customers and manage operations.

The appeal is clear: IoT solutions give banks real-time insights into customer behavior, help detect fraud faster, and streamline everyday processes. This makes the banking Internet of Things not just a technological upgrade but a strategic necessity.

In this blog, we’ll explore existing IoT use cases already transforming banking and take a closer look at what the future holds as IoT technology continues to evolve.

IoT in banking refers to the use of connected devices, sensors, and smart technologies to collect and analyze data in real time, making financial services faster, safer, and more personalized. In simple terms, it means that everyday objects—like ATMs, wearable devices, or even cars—can be linked to a bank’s digital systems to enable secure transactions and deliver smarter customer experiences.

The integration of IoT technology in financial services goes beyond payments. Banks can use sensors to monitor ATM performance, track customer behavior through mobile devices, or connect with smart home assistants to allow voice-enabled banking. This creates a seamless bridge between physical devices and digital banking platforms.

The key benefits of IoT banking include:

In short, the Internet of Things in banking transforms traditional services into connected, data-driven experiences that enhance security, convenience, and efficiency for both banks and their customers.

The Internet of Things in banking is no longer just an emerging trend—it’s a strategic tool that banks are using to stay competitive. From improving customer engagement to strengthening security, IoT offers practical solutions that reshape how financial institutions operate.

One of the biggest drivers of IoT adoption in banking is the ability to deliver highly personalized services. By analyzing real-time data from connected devices, banks can provide financial insights tailored to individual spending patterns. For example, customers might receive instant savings tips based on their transactions or alerts about unusual activity.

IoT also enables location-based services, such as guiding customers to the nearest branch or ATM with the shortest wait time. In smart branches, sensors can streamline navigation, making the banking experience more efficient and customer-friendly.

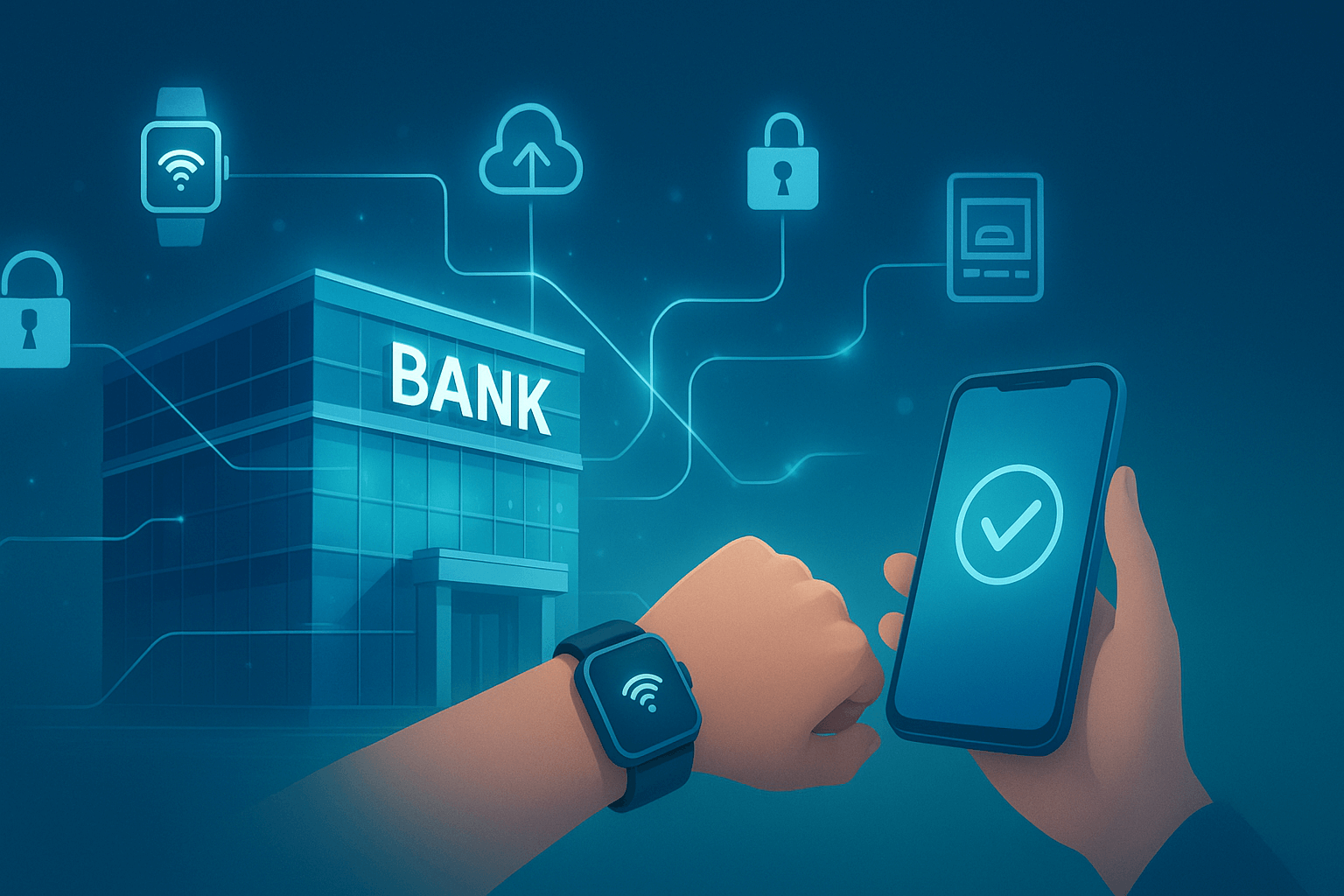

Security is at the core of modern banking, and IoT is helping institutions add stronger layers of protection. Biometric authentication through smart devices—such as fingerprints, facial recognition, or wearable-based verification—offers a faster and safer way to access accounts.

Beyond authentication, IoT-powered fraud detection allows banks to monitor transactions in real time. Connected systems can flag unusual spending behavior instantly, reducing the risk of fraud and giving customers more confidence in digital banking services.

For banks, efficiency is just as important as customer satisfaction. IoT makes it possible to run operations more smoothly by reducing downtime and lowering costs. Smart ATMs equipped with IoT sensors can predict maintenance needs before machines fail, minimizing service disruptions.

Inside branches, IoT helps with resource allocation by tracking customer flow and staff availability. This ensures that employees are placed where they’re needed most, improving service quality and reducing wait times.

Banks are already leveraging the Internet of Things in banking to modernize services, cut costs, and improve customer experiences. Several real-world applications show how IoT is reshaping day-to-day financial operations.

Traditional ATMs often fail without warning, causing frustration for customers and higher maintenance costs for banks. With IoT-enabled ATMs, sensors can track performance and trigger predictive maintenance alerts before a breakdown occurs. This reduces downtime and ensures reliable service.

Inside branches, IoT technology is being used for queue management and foot traffic analysis. Sensors help banks monitor customer flow in real time, allowing them to optimize staffing and reduce wait times. The result is a smoother, more efficient branch experience.

Wearables such as smartwatches are becoming powerful tools in banking. Customers can use IoT-enabled devices to make instant contactless payments, check balances, or receive account alerts without pulling out their phones.

Banks also use personalized notifications and real-time monitoring to provide customers with insights on spending habits, low balance warnings, or fraud alerts—delivered directly to their wrist.

Automotive IoT is opening new opportunities for financial institutions. Many banks are partnering with car manufacturers to support in-car payment systems for tolls, parking, and fuel. Drivers can pay without using cash or cards, making transactions faster and safer.

These partnerships between banks and automotive companies highlight how IoT extends financial services beyond branches and mobile apps, embedding banking into everyday life.

The insurance sector, closely tied to banking, is also adopting IoT to improve risk analysis. Usage-based insurance models use IoT devices like telematics in cars or wearables in health insurance to assess individual behavior and offer customized premiums.

IoT further enables real-time risk assessments, allowing insurers to monitor driving patterns, lifestyle habits, or property conditions. This data-driven approach helps banks and insurers provide fair pricing while reducing fraud and claims disputes.

While IoT is already making an impact, its potential in financial services is far from fully realized. The Internet of Things in banking is set to deliver even more advanced applications that could redefine how customers interact with their money and how banks manage security, efficiency, and personalization.

As smart homes become mainstream, banking is expected to integrate seamlessly with connected devices. Imagine using voice-activated assistants like Alexa or Google Home to authorize payments, check balances, or transfer funds.

IoT sensors will also enable automated bill payments, where devices like smart meters could trigger direct payments for electricity, water, or internet bills as usage is recorded—eliminating manual scheduling and reducing missed payments.

Fraud prevention will evolve with the combination of AI and IoT. Banks will be able to detect anomalies in user behavior across multiple devices, flagging unusual activity in real time.

A multi-device authentication ecosystem—where identity verification happens across wearables, smartphones, and biometric devices—will strengthen security without adding complexity for customers. This layered approach will make it harder for cybercriminals to bypass defenses.

IoT wearables could soon play a bigger role in financial wellness. By analyzing spending habits alongside lifestyle data, such as fitness or travel patterns, banks can provide highly personalized advice.

Instead of generic notifications, customers may receive proactive financial guidance—for example, alerts about overspending trends or savings opportunities linked to daily activities. This level of personalization could make banking more consultative and customer-centric.

The combination of blockchain and IoT in banking promises secure, transparent, and tamper-proof financial transactions. IoT devices could execute payments automatically on blockchain networks, ensuring accuracy and reducing the risk of fraud.

This innovation also paves the way for cross-border IoT payments, where connected devices can handle international transactions instantly and at lower costs. Such systems could remove many of the delays and fees that currently limit global financial interactions.

While the Internet of Things in banking offers significant opportunities, adoption comes with serious challenges. Banks must overcome these hurdles to fully realize the value of IoT solutions.

IoT devices generate massive amounts of customer data, from transaction history to location details. Protecting this data is a top priority. Any vulnerability in connected devices can expose sensitive information, making cybersecurity in IoT banking a critical concern. Banks must invest in robust encryption, secure networks, and continuous monitoring to safeguard against breaches.

Building a strong IoT ecosystem requires significant investment. Banks need to upgrade legacy systems, deploy smart devices, and integrate real-time data platforms. These infrastructure costs can be high, especially for large networks of ATMs, branches, and mobile channels. Smaller banks may struggle to compete without strategic partnerships or phased adoption.

Financial institutions operate under strict regulations. With IoT, compliance becomes more complex as customer data flows across multiple devices and networks. Regulators require strict adherence to data protection and privacy laws, which can slow down IoT deployment. Banks must strike a balance between innovation and compliance to avoid penalties.

Even with advanced IoT solutions, customer adoption depends on trust. Many people remain cautious about sharing personal data across multiple devices. Concerns about surveillance, misuse of data, or device failures can discourage adoption. To succeed, banks must demonstrate transparency, educate customers, and show the real benefits of IoT in banking services.

The banking Internet of Things is set to grow rapidly in the next decade as financial institutions continue to integrate connected devices into their services. Over the next 5–10 years, IoT will likely move from experimental projects to mainstream banking operations, reshaping everything from customer service to fraud detection.

IoT will expand beyond ATMs and wearables into every aspect of digital finance. Branches may rely fully on connected systems to manage customer flow, while mobile banking apps will use IoT-driven data for more accurate financial recommendations. Banks that invest early will be able to deliver seamless, data-driven services that customers expect.

IoT’s success will depend on complementary technologies. AI will analyze massive IoT data sets to detect fraud, predict customer needs, and automate decisions. 5G networks will enable faster, more reliable communication between connected devices, powering real-time banking transactions. Meanwhile, blockchain will provide the security and transparency needed for IoT-based payments and contracts. Together, these technologies will create a stronger, safer, and more efficient IoT ecosystem for banking.

Banks that act quickly on IoT adoption will gain a long-term advantage. Early adopters can reduce costs through predictive maintenance, build customer loyalty with personalized services, and strengthen security with multi-device authentication. As the Internet of Things in banking becomes standard, these institutions will already have the infrastructure, expertise, and trust to lead the market.

Conclusion

The Internet of Things in banking is no longer a distant concept—it is already shaping how financial institutions operate and serve customers. Today, IoT powers smart ATMs, wearable banking, connected cars, and usage-based insurance models. Looking ahead, innovations such as voice-activated payments, real-time fraud prevention, IoT-driven financial health tracking, and blockchain-enabled transactions will take banking efficiency and security to new levels.

What was once a convenience is quickly becoming a necessity. Banks that fail to adapt risk falling behind as customer expectations shift toward personalized, data-driven, and secure services.

For banks, fintech leaders, and decision-makers, now is the time to explore IoT-driven strategies. By investing in IoT banking solutions, institutions can improve customer trust, strengthen security, and position themselves at the forefront of the digital banking revolution.